VAT exemption for foreigners in Turkey is the tax relief mechanism under Article 13/i of VAT Law No. 3065 that removes the VAT obligation on qualifying new-build property purchases made by eligible foreign nationals and Turkish citizens residing abroad, provided the payment is transferred in foreign currency and the property is retained for a minimum of three years.

Most foreign investors approach a Turkish property transaction focused on what is immediately visible: the purchase price, the projected rental yield, the citizenship threshold. The tax structure beneath the transaction receives less attention. That gap between the surface of the deal and its legal architecture is precisely where many applications fail, and where the difference between a correctly structured purchase and a procedurally defective one becomes measurable.

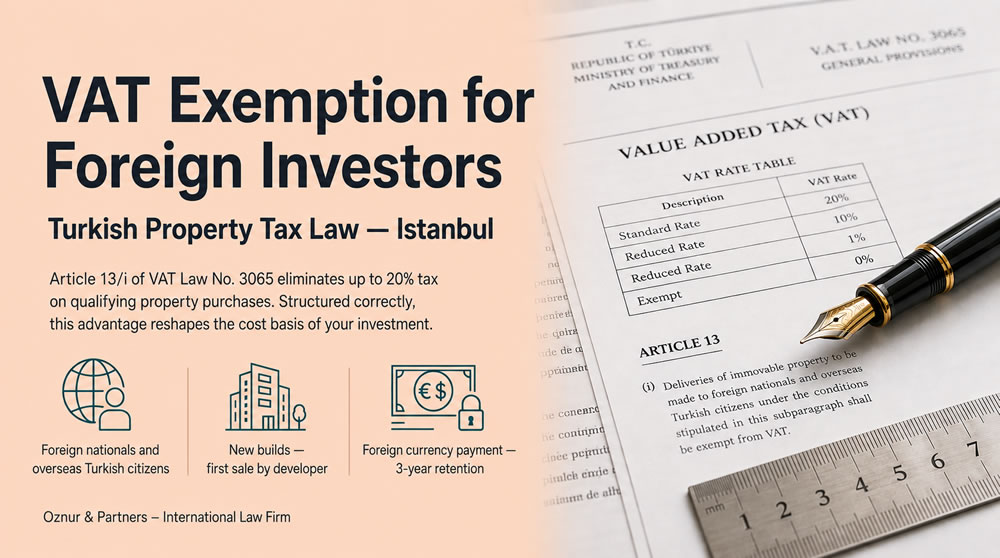

What makes this exemption valuable is not only the rate it eliminates. Under current regulations, VAT on new residential property ranges from 1% to 20% depending on permit date, location and floor area. For a property purchased at USD 300,000 with a 10% rate, the exemption represents USD 30,000 in avoided cost. At 20%, the same investment produces a USD 60,000 saving. These figures alter the cost basis of the investment from the point of acquisition, and they are available only to buyers who satisfy every procedural condition, in the correct sequence, before the title deed transfer takes place.

⚖️ Who Qualifies for VAT Exemption in Turkey — and Who Does Not?

Eligibility under Article 13/i is determined by residency status, not nationality. The distinction matters because a foreign passport alone does not confer the exemption.

The following categories qualify:

- Foreign nationals who have not resided in Turkey during the six months prior to the purchase date

- Turkish citizens who hold a valid work or residence permit and have been living abroad continuously for at least six months

- Foreign companies that do not maintain a permanent establishment, branch or representative office in Turkey

The following are not eligible:

- Foreign nationals currently residing in Turkey, regardless of their citizenship

- Foreign companies registered as taxpayers in Turkey

The six-month non-residency condition is verified against official entry-exit records held by the Turkish authorities. A buyer who has been spending extended periods in Turkey — even without formal registration — may face scrutiny at the documentation stage. This is why proof of non-residency is among the first documents a legal advisor will request, not the last.

*This is precisely why foreign investors increasingly ask: does owning a holiday home in Turkey affect eligibility?* The answer depends on whether that ownership has been accompanied by stays that, cumulatively, trigger residency status. The threshold is formal and documentable, not a matter of perception.

⚖️ Which Properties Are Covered — and What Falls Outside the Exemption?

The exemption applies exclusively to newly constructed residential or commercial units sold for the first time by a developer or construction company. This definition excludes a significant portion of the Turkish property market.

Qualifying properties:

- Newly built apartments, villas, offices and shops sold directly by the developer

- Units with an issued occupancy permit (iskan) ready for title deed transfer

- Properties sold under a kat irtifakı (construction easement) arrangement, provided the unit is ready for delivery

Properties that do not qualify:

- Resale transactions between private parties

- Second-hand commercial or residential units, regardless of their age

- Land parcels without a residential or commercial construction permit

The first-sale requirement is enforced at the invoice stage. The developer issues an invoice explicitly referencing Article 13/i of Law No. 3065, confirming the sale is exempt. If that notation is absent, the exemption cannot be applied or reinstated after the fact. Buyers who discover this omission after title deed transfer have no recourse.

⚖️ Core Conditions of the Exemption

Three requirements must be satisfied simultaneously. A failure in any one of them voids the exemption entirely.

Foreign currency payment from abroad. At least 50% of the purchase price must be transferred to Turkey in foreign currency from an account held outside Turkey. The transfer must be traceable through the Turkish banking system, with the bank receipt confirming the origin of the funds. Transfers from Turkish bank accounts, even if denominated in foreign currency, do not satisfy this condition under current Revenue Administration practice.

First-hand sale by developer. The property must be purchased directly from the construction company or developer that built it. A resale by any intermediary, even shortly after the developer’s original sale, disqualifies the transaction.

Three-year retention. Law No. 7394, effective 1 May 2022, extended the minimum holding period from one year to three years. The property cannot be sold, transferred or otherwise disposed of within three years of the title deed registration date. This restriction is not a contractual obligation between buyer and seller; it is recorded as a legally binding annotation on the title deed itself, enforceable by the tax authority. If the property is sold before three years have elapsed, the VAT that was not collected at the time of purchase becomes immediately payable, together with interest calculated under Article 48 of Law No. 6183. The liability falls on the person who originally purchased under the exemption.

⚖️ Updated VAT Rates (2026)

Turkey’s standard VAT rate has been 20% since July 2023, increased from the previous 18%. The rate applicable to a specific property depends on three variables: the date of the building permit, the size of the unit, and in metropolitan areas, the land value per square metre.

| Permit Date | Property Size | VAT Rate |

|---|---|---|

| After 1 April 2022 | Below 150 m² | 10% |

| After 1 April 2022 | Above 150 m² | 10% for first 150 m², 20% for the remainder |

| 1 January 2013 to 31 March 2022 | Below 150 m² | 1% |

| 1 January 2013 to 31 March 2022 | Above 150 m², non-metropolitan | 20% |

| 1 January 2013 to 31 March 2022 | Above 150 m², metropolitan, land value below 1,000 TL/m² | 1% |

| 1 January 2013 to 31 March 2022 | Above 150 m², metropolitan, land value 1,000 to 1,999 TL/m² | 10% |

| 1 January 2013 to 31 March 2022 | Above 150 m², metropolitan, land value above 2,000 TL/m² | 20% |

| Urban transformation / risky buildings | Below 150 m² | 1% |

| Urban transformation / risky buildings, permit before 1 April 2022 | Above 150 m² | 20% |

| Urban transformation / risky buildings, permit after 1 April 2022 | Above 150 m² | 10% for first 150 m², 20% for the remainder |

For a new 120 m² apartment in Istanbul with a post-April 2022 building permit, the applicable rate is 10%. A buyer who qualifies under Article 13/i and structures the transaction correctly eliminates that 10% entirely.

⚖️ Application Process: Step by Step

The exemption is applied at the point of transaction, not claimed retroactively. Every step must be completed in the correct sequence before the title deed transfer.

- Obtain a Turkish Tax Identification Number. Required for all banking and Land Registry transactions. Can be obtained at any tax office in Turkey or, for buyers not present in Turkey, through a notarised Power of Attorney. The process takes one working day.

- Transfer the purchase amount from abroad. At least 50% of the agreed price must arrive in Turkey in foreign currency from an account held outside the country. The bank receipt, showing the originating account and the amount, is submitted as primary documentation at the Land Registry.

- Sign a notarised sales agreement. The contract must state that the transaction is being concluded under VAT exemption pursuant to Article 13/i of Law No. 3065. An agreement that omits this reference cannot be used to support an exemption claim.

- Developer issues a VAT-exempt invoice. The invoice must explicitly cite Article 13/i. The Revenue Administration now requires developers to declare VAT exemptions electronically through the GIB system; the buyer should confirm this has been done before proceeding to the Land Registry.

- Complete title deed registration. At the Land Registry Office (Tapu Müdürlüğü), the developer formally notifies the office that the transaction is exempt under Article 13/i. The three-year retention restriction is recorded as an annotation on the deed at this stage.

- Obtain the VAT Exemption Certificate. Issued by the relevant Tax Office upon confirmation of the transfer and documentation.

The entire process, from Tax Identification Number to title deed transfer, typically takes between one and three weeks, depending on the workload of the Land Registry Office and whether all documents are prepared in advance. Transactions where the buyer is not physically present in Turkey are completed through a Power of Attorney, which is prepared in the buyer’s country of residence, apostilled under the Hague Convention and translated by a sworn translator.

⚖️ Required Documents

- Passport, with notarised Turkish translation

- Turkish Tax Identification Number certificate

- Official proof of non-residency in Turkey (entry-exit record or certificate from the relevant authority)

- Bank transfer receipt confirming foreign currency payment from an account held abroad

- Notarised sales agreement referencing Article 13/i of Law No. 3065

- VAT-exempt invoice issued by the developer

- Title deed registry document

⚖️ VAT Exemption and Turkish Citizenship by Investment

The VAT exemption and the Turkish citizenship by investment program are separate legal frameworks that can be pursued simultaneously when the transaction is structured to satisfy both.

A property purchased under Article 13/i can qualify for the citizenship program provided the following additional conditions are met:

- The declared value of the property is at least USD 400,000, confirmed by a valuation report from a licensed appraiser authorised by the Ministry of Environment, Urbanization and Climate Change

- The investment is retained for a minimum of three years

- Payment is made through a Turkish bank in foreign currency

The structural overlap between the two programs is significant. Both require a three-year retention period and foreign currency payment via the banking system. An investor who plans the transaction from the outset to satisfy both sets of conditions can pursue citizenship eligibility without bearing the 10% or 20% VAT cost that would otherwise apply.

VAT exemption does not confer citizenship. It reduces the cost of an investment that may, if additional criteria are met, support a citizenship application. The sequence matters: the exemption conditions must be satisfied at the time of purchase; the citizenship application is filed after the investment is made and documented.

*Sophisticated investors routinely ask: which transaction structures allow both the tax exemption and the citizenship pathway to be pursued from a single property purchase?* The answer depends on the property value, permit date and the buyer’s residency status — variables that should be assessed before any agreement is signed.

⚖️ VAT Exemption and Citizenship: Comparison

| Criterion | VAT Exemption | Citizenship by Investment |

|---|---|---|

| Minimum investment | No minimum threshold | USD 400,000 in real estate |

| Tax benefit | Up to 20% VAT eliminated | No tax exemption; grants long-term residence rights |

| Retention period | 3 years (since 1 May 2022) | 3 years |

| Payment requirement | Foreign currency from abroad via Turkish bank | Foreign currency via Turkish bank |

| Eligible property | New builds only, first sale by developer | New or resale, subject to valuation report |

| Processing time | Applied at point of transaction | Typically 3 to 6 months from application |

⚖️ Common Mistakes That Void the Exemption

Applications fail for predictable reasons. The three most frequent errors carry no remedy after the fact.

Payment currency and source. Funds transferred from a Turkish bank account, even one held in a foreign currency, do not satisfy the requirement. The origin of the transfer matters as much as its denomination. This is checked against the bank receipt at the Land Registry and cannot be corrected retrospectively.

Invoice omission. The developer’s invoice must explicitly reference Article 13/i of Law No. 3065. If the invoice is issued without this notation — whether by oversight or because the developer’s sales team did not process the exemption correctly — the buyer has no basis for claiming the relief. The Revenue Administration’s requirement that developers declare exemptions electronically through GIB adds an additional verification layer that a real estate lawyer in Turkey will confirm before the title deed transfer proceeds.

Early disposal. Selling, gifting or otherwise transferring the property within three years of the title deed registration date triggers immediate repayment of the avoided VAT plus accrued interest. The annotation on the title deed makes this obligation visible to any buyer in a subsequent transaction, and the liability cannot be assigned or waived by agreement between the parties.

⚖️ Working with a Turkish Property Lawyer on a VAT Exemption Transaction

The exemption exists in law, but its application is procedural. Each condition has a timing requirement, a documentation standard and a sequence dependency. A payment that arrives after the agreement is signed but before the invoice is issued may satisfy the requirement or may not, depending on how the Revenue Administration interprets the transfer documentation. An invoice issued without the Article 13/i reference cannot be reissued after the fact.

These are not edge cases. They are the routine friction points of a process that moves through multiple institutions, each with its own documentation requirements, and where the window for correction closes at the point of title deed registration.

*It is no coincidence that international investors compare jurisdictions and ask: which Turkish property purchase structures genuinely eliminate VAT, and which create the appearance of a saving that is later reversed?* The answer lies in the procedural detail, not the legal principle.

What appears to be a straightforward administrative process is, from the Revenue Administration’s perspective, a verification of residency status, payment origin, invoice accuracy and retention commitment. Correct preparation means each of these verification points is satisfied before it is examined, not after.

Schedule a Legal Consultation

If you are assessing a property purchase in Turkey, evaluating VAT exemption eligibility, or considering a combined investment and citizenship structure, our Investment Lawyers in Istanbul are available for an initial consultation to review your specific situation.

❓ Frequently Asked Questions

✅ What is the VAT exemption for foreigners buying property in Turkey?

The VAT exemption for foreigners in Turkey is a tax relief under Article 13/i of VAT Law No. 3065, which eliminates VAT on qualifying new-build property purchases made by eligible foreign nationals or Turkish citizens residing abroad. To benefit, the buyer must not reside in Turkey, pay at least 50% of the price in foreign currency transferred from abroad, and retain the property for a minimum of three years from title deed registration.

✅ Which VAT rate is eliminated by the exemption?

The rate eliminated depends on the building permit date and property size. For properties with permits issued after 1 April 2022, the rate is 10% for units below 150 m² and a blended 10%/20% for larger units. Properties with permits issued between 2013 and March 2022 may carry rates of 1%, 10% or 20% depending on location and land value. The exemption removes whichever rate would otherwise apply.

✅ Can the VAT exemption be used more than once by the same buyer?

There is no statutory limit on the number of qualifying transactions. Each purchase is assessed independently: a new property, new payment documentation confirming foreign currency transfer from abroad, and documented non-residency at the time of each purchase. The conditions must be satisfied separately for each transaction.

✅ What happens if the property is sold within three years?

If the property is sold, transferred or otherwise disposed of within three years of title deed registration, the VAT that was not collected at the time of the original purchase becomes immediately payable, together with interest calculated under Article 48 of Law No. 6183. This obligation is recorded on the title deed as an annotation at the time of purchase and cannot be waived by agreement between buyer and seller.

✅ Does the exemption apply to resale properties?

No. Article 13/i applies only to new-build properties sold for the first time by the developer. Resale transactions between private parties are excluded regardless of the buyer’s residency status, payment method or the age of the property.

✅ Can a property purchased under VAT exemption also be used for a citizenship application?

Yes, provided the property meets the separate requirements of the citizenship program: a declared value of at least USD 400,000 confirmed by an authorised valuation report, and a three-year retention commitment. Both programs share the same core conditions of foreign currency payment and three-year retention, which means a single correctly structured transaction can satisfy both sets of requirements simultaneously.

✅ Does the payment need to originate from outside Turkey?

Yes. The foreign currency transfer must originate from an account held outside Turkey and arrive through the Turkish banking system. Transfers from accounts already held in Turkey, even in foreign currency, do not satisfy the requirement under current Revenue Administration practice. The bank receipt must confirm both the foreign origin and the amount.

✅ What is the minimum property value for the VAT exemption?

There is no minimum investment threshold for the VAT exemption itself. Any qualifying new-build property purchase, regardless of value, can benefit from Article 13/i provided the residency, payment and retention conditions are met. The USD 400,000 minimum applies only to the Turkish citizenship by investment program.

✅ How long does the VAT exemption process take?

From obtaining a Tax Identification Number to title deed transfer, the process typically takes between one and three weeks, depending on document preparation, Land Registry workload and whether the buyer is present in Turkey. Transactions completed through a Power of Attorney, where the buyer does not travel to Turkey, follow the same timeline once the POA has been apostilled and submitted.

✅ Which official regulation governs this exemption?

The exemption is governed by Article 13/i of Turkish VAT Law No. 3065, introduced in 2017 to encourage foreign real estate investment. The three-year retention period was extended from one year to three years by Law No. 7394, effective 1 May 2022. The implementing communiqué is the KDV Genel Uygulama Tebliği (VAT General Application Communiqué), Series 42, issued by the Ministry of Treasury and Finance. The original regulation was published in the Official Gazette on 5 May 2017.

⚖️ Related Legal Resources

🔹 Citizenship and Investment

Foreign Investment and Citizenship Law — Overview of the legal framework governing investment-based citizenship applications in Turkey, including the USD 400,000 real estate threshold, eligible investment routes and the 3-to-6-month processing timeline.

Turkish Citizenship Lawyer — Legal guidance on the citizenship by investment process, application structure, document requirements and common procedural errors that delay or void applications.

Turkish Citizenship by Investment: 2026 Regulatory Updates — Current status of regulatory changes affecting the citizenship program, including valuation standards and processing authority updates.

🔹 Real Estate and Property Law

Real Estate Lawyer in Turkey — Legal representation for property acquisitions, title deed due diligence, developer contract review and Land Registry transactions across Turkey.

Property Lawyers in Turkey — Guidance on structuring property purchases for foreign buyers, including Power of Attorney procedures, valuation report requirements and post-acquisition compliance.

🔹 Tax and Compliance

KDV İstisnası ve Nakit Beyan Formu — Turkish-language overview of the VAT exemption and the cash declaration form requirement for foreign currency brought into Turkey.

Turkey 20-Year Tax Exemption 2026 — Legal analysis of the income tax exemption available to individuals returning to Turkey from abroad, a separate incentive that may apply concurrently with the VAT exemption for certain buyers.

The three-year clock that starts on the day of title deed registration is not a contractual arrangement that can be renegotiated. It is a lien on the property, visible to every subsequent buyer and enforceable by the tax authority. Investors who understand this from the outset plan their holding period accordingly. Those who discover it after the fact find the options narrower than they expected.

The exemption itself is well-designed: it is accessible, it is substantial, and it is available across all property categories and locations in Turkey. What it requires, in return, is that every procedural condition be satisfied before the title deed transfer. Not after. Not approximately. Before.